Meta Just Beat Google in Global Ad Revenue: A Case for Demand Diversification

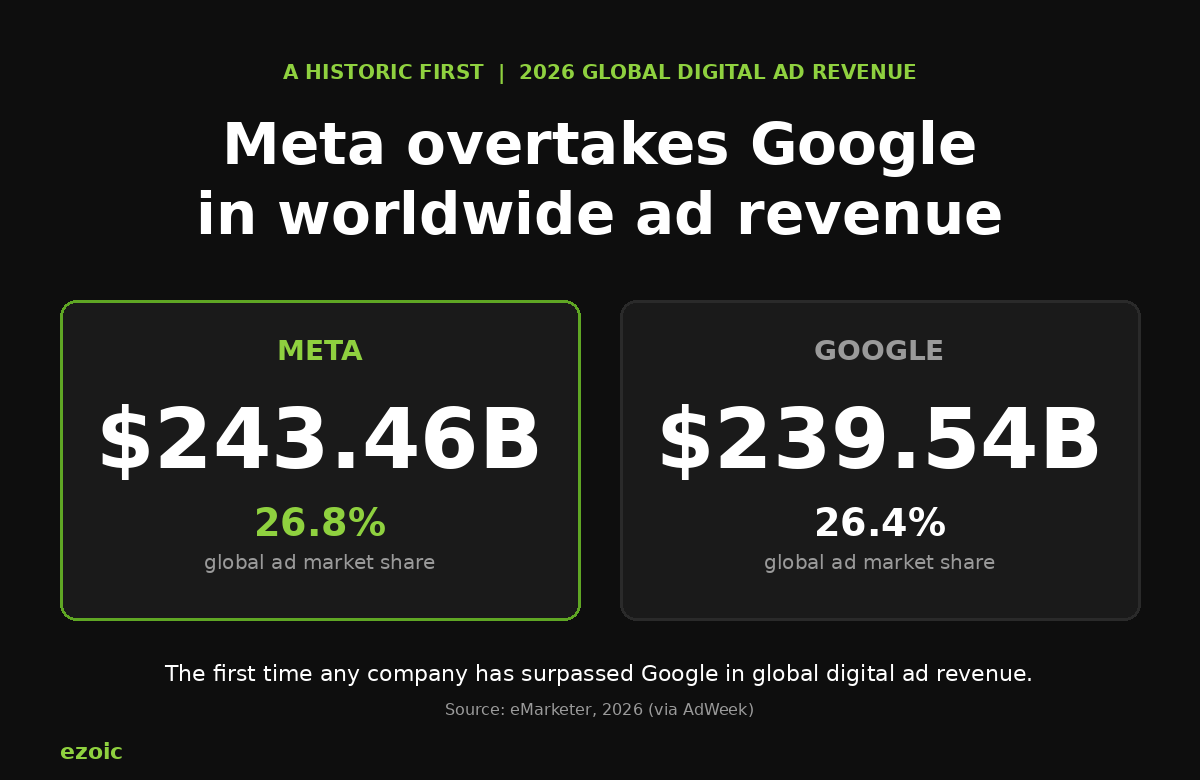

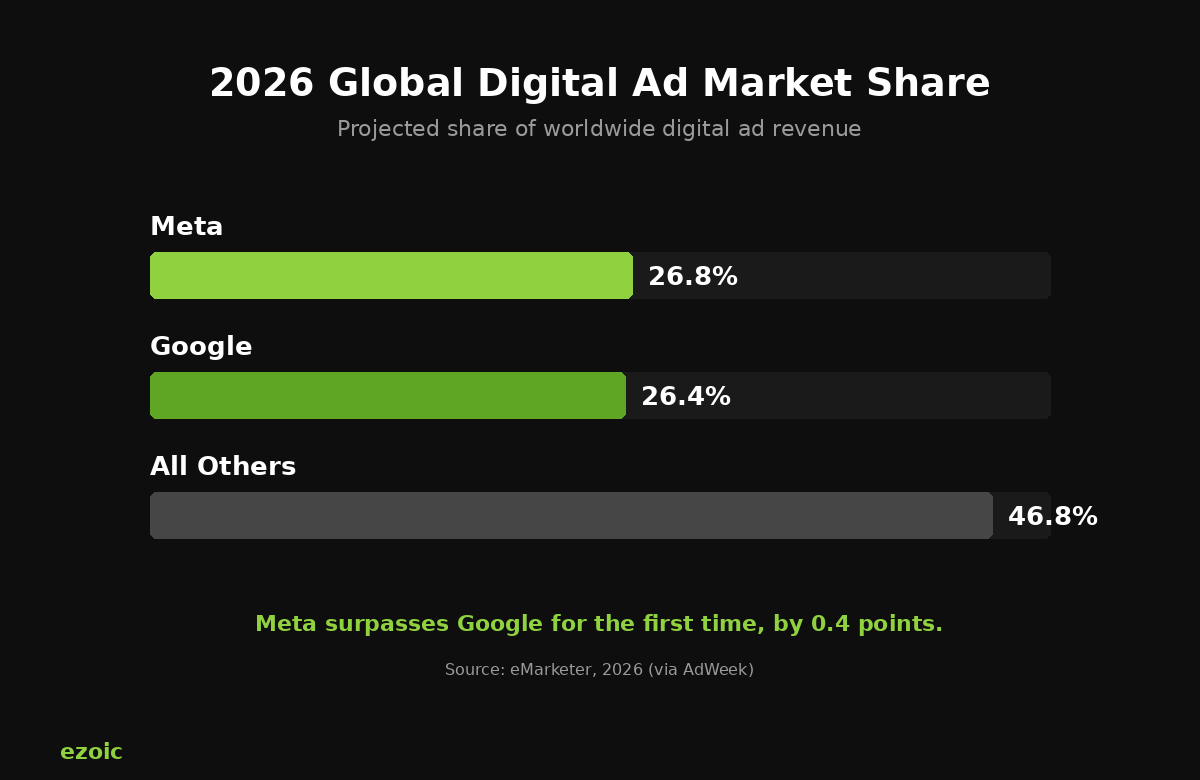

For the first time in the history of digital advertising, Meta is projected to pass Google as the largest digital ad business in the world. Per eMarketer data reported by AdWeek, Meta is on track for $243.46B in global ad revenue in 2026, edging Google's $239.54B, a 26.8% vs. 26.4% global share split. The scoreboard matters less than what's underneath it: advertiser dollars are moving to platforms that pair scale with automation and measurable return on ad spend, and the open web is feeling the pull. For any digital business with revenue tied to a single Google-driven demand path, this is the moment to re-evaluate the shape of the ad stack.

The Handoff: What Actually Happened

This isn't a one-quarter blip. eMarketer's forecast has Meta capturing a larger slice of global ad revenue than any single company, ever, fueled by Reels monetization, AI-assisted creative and bidding (Advantage+), and a merchant base that keeps deepening its reliance on Meta's targeting graph. Google still owns Search, YouTube, and a programmatic stack embedded in roughly half the open-web supply chain, but its share is compressing while Meta's expands.

The open-web context matters just as much as the headline. Basis peg US programmatic display spend on track to exceed $203B in 2026, growing 12.5% year-over-year after 13.6% growth in 2025. Dollars into the open web are still rising. They're just being allocated differently: toward cleaner supply, better signals, and infrastructure that lets a buyer reach an identified audience efficiently.

Why a 0.4-Point Share Shift Is Actually a Structural Signal

A four-tenths-of-a-point market share flip doesn't sound dramatic. The durable read is different: the gravitational center of paid media is migrating to platforms that bundle demand, audience, and measurement in a single closed loop. Every dollar spent inside Meta is a dollar that didn't contest an open-auction impression. Over time, that reshapes both the volume and the character of demand reaching the open web.

Three effects are already visible in the data:

- Demand concentration risk is rising for operators dependent on a single SSP or AdSense-only stacks. If Google's share is compressing while Meta's is closing, the old default of "Google handles it" no longer covers the full demand picture.

- Buyer scrutiny on supply quality is tightening. Jounce Media's April 2026 supply path benchmarking put aggregate bidstream transparency at 97.6%, and buyers are demonstrating a measurable directness bias, paying premiums for clean, authorized paths and discounting everything else.

- Identity is becoming the admission ticket to premium demand. Per eMarketer, 85% of publishers expect first-party data's role in monetization to grow further in 2026, and properties pairing first-party data with AI-driven segmentation are seeing CPM uplifts of 20-50%.

The uncomfortable translation: a narrow demand stack and a thin identity layer are now the two most expensive decisions an operator can make.

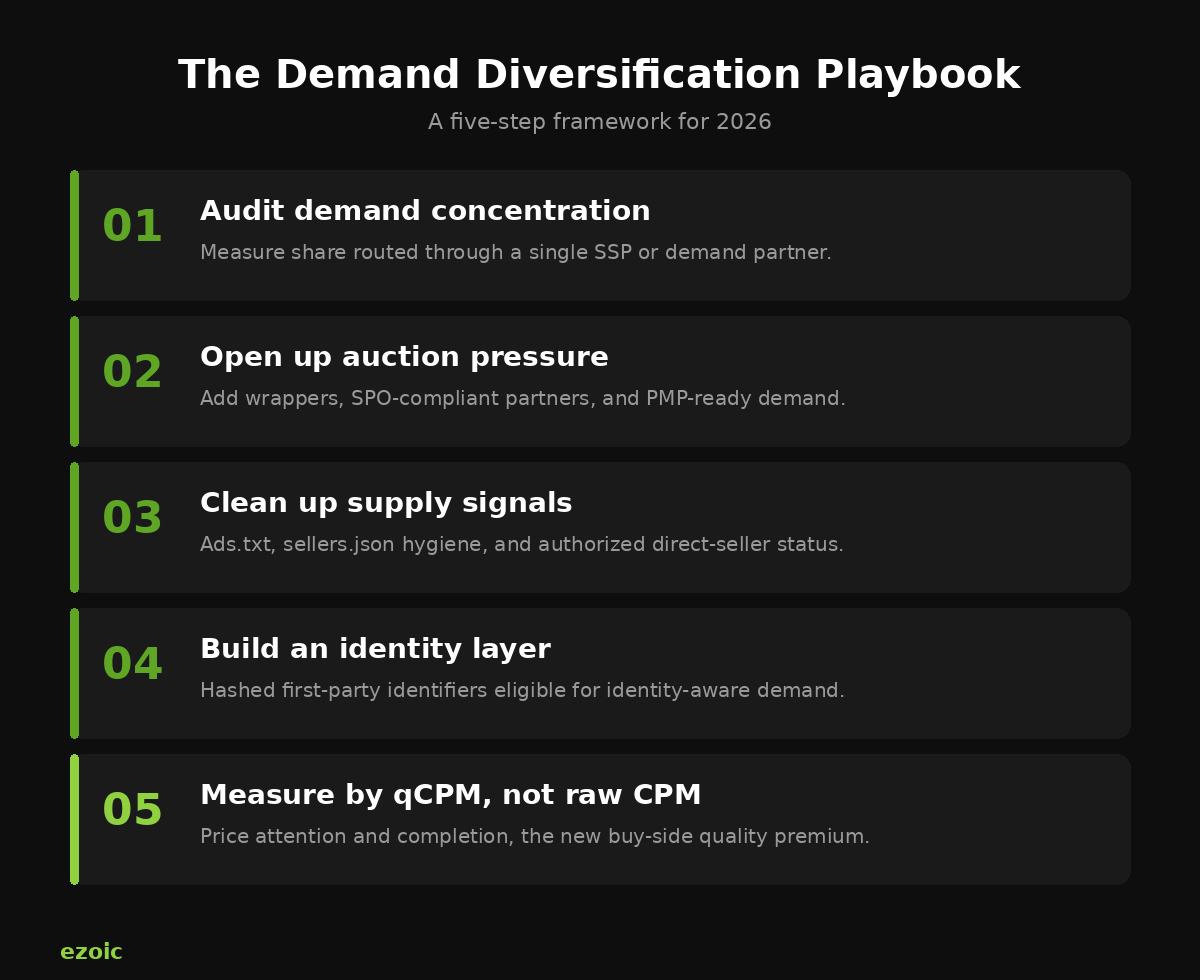

The Demand Diversification Playbook

Diversifying demand isn't a matter of adding partners for the sake of adding partners. It's a matter of making sure impressions are competing inside a broader set of auctions, with more advertisers, and under signals that buyers actually want to bid against. A useful framework for 2026:

- Audit demand concentration. What share of programmatic revenue is routed through a single SSP or demand partner? If one partner represents more than 60%, the business is structurally exposed to any shift in that partner's auction dynamics, take rate, or demand mix. (For a fuller look at how the stack has evolved, see the systems Ezoic has been building.)

- Open up auction pressure. Adding header bidding wrappers, SPO-compliant demand partners, and PMP-ready demand increases the number of advertisers contesting each impression. That is the single most reliable way to raise clearing prices.

- Clean up supply signals. Ads.txt and sellers.json hygiene, authorized direct-seller status, and eliminating rebroadcast paths all feed the directness premium buyers are now paying, per Jounce Media's 2026 benchmarking.

- Build an identity layer buyers can bid against. Logged-in users, newsletter signups, and hashed first-party identifiers are what make an impression eligible for the identity-aware demand that's increasingly where higher CPMs live.

- Measure by qCPM, not raw CPM. Attention and completion metrics are becoming pricing inputs on the buy side. Operators measuring only raw CPM are missing the quality premium that clean, identified inventory now commands.

Pro tip: The first diversification move most operators skip is the simplest one: pulling a concentration report. Without a known top-partner share, the exposure can't be managed.

Where EzoicAds Fits

EzoicAds is built for exactly this problem. It brings a diversified set of SPO-compliant demand partners (e.g. The Trade Desk via OpenPath and OpenAds) into a single auction so every impression is contested by the broadest possible pool of advertisers. For a digital business sitting on a Google-heavy stack, that's the mechanical answer to concentration risk. For a larger operator already running a bidding wrapper, it's incremental auction pressure plus a cleaner path to buyers who are rewarding directness.

Pair that with ezID, Ezoic's first-party identity layer, and the picture tightens further. ezID hashes publisher-collected identifiers (logged-in emails, newsletter subscribers, quiz-captured leads) and passes them into the bid request, making impressions eligible for identity-aware demand that consistently prices above anonymous inventory. That combination of diversified demand plus a clean identity signal is what turns the Meta vs. Google headline from a threat into a planning prompt.

What Comes Next

The Meta-over-Google moment won't reverse in 2026. Platform-level demand will keep concentrating wherever closed-loop measurement and automation exist, and the open web will keep earning its share on the strength of supply quality and audience signal. Operators who treat this as a one-time news item will still be here a year from now, wondering why their CPM curve flattened. Operators who use it as a prompt to audit demand concentration, open up auction pressure, and build a real identity layer will enter 2027 with a structurally more resilient revenue base.

The headline is the historic part. The playbook is the operational part. Publishers, platforms, and digital businesses who run the playbook this quarter are the ones who'll be hardest to displace when the next share shift lands.